I turn stochastic calculus, statistics and numerical methods into trading and risk models that hold up out-of-sample. Open to freelance projects in quantitative modeling, risk analysis, and time series forecasting.

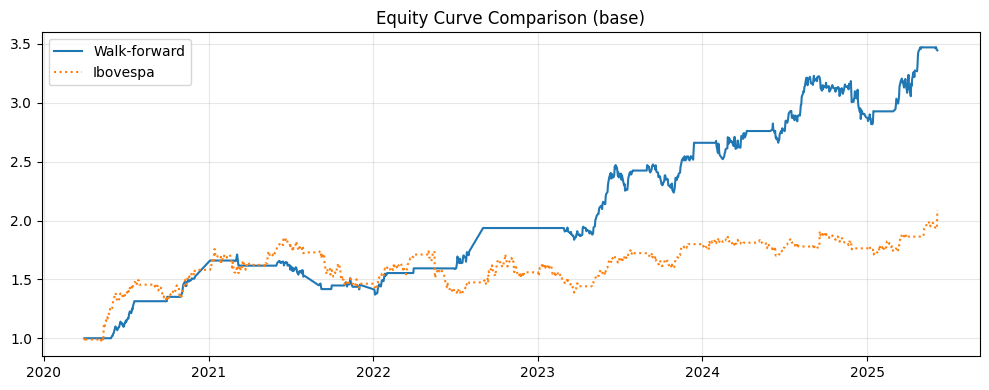

📈 Atlas — regime-aware equity strategy · Itaú Quant Challenge 2025, top 4% (40/953) · Long-only Ibovespa strategy: regime detection via topological data analysis, factor meta-models (Ridge/ElasticNet), regime-sensitive HRP allocation. Out-of-sample Sharpe 1.18 vs 0.55 benchmark · Sortino 1.90 · validated with a Deflated Sharpe test.

🤖 Titanium Alpha — agentic multi-strategy fund · Four LLM agents (LangGraph) debate PatchTST forecasts and RAG-retrieved news before capital is allocated via HRP with Ledoit–Wolf shrinkage. 1,000+ tests, CI, CPCV grid search over 547 configs. 10-year walk-forward (52 S&P 500 names): Sharpe 0.77 vs SPY 0.59, max drawdown −22% vs −34%.

🧮 Mean Field Games for market microstructure · undergraduate research, UFRJ · Numerically solves the coupled HJB–Fokker–Planck system (finite differences + Picard iteration) to model HFT ↔ market-maker dynamics, calibrated on B3 data. Shows liquidity resilience and liquidity-crunch regimes emerging from agent interaction alone.

Python (NumPy · SciPy · pandas · scikit-learn · LangGraph) · SQL · backtesting with purged CV · portfolio optimization (HRP, Markowitz) · time series (ARIMA/GARCH, PatchTST) · stochastic calculus & numerical PDEs

More in the pinned repos below · LinkedIn · felipe.cockles@hotmail.com